Upcoming Changes to Social Security in 2022

Upcoming Changes to Social Security in 2022 Social Security has provided a financial foundation for our nation’s retired employees since it was enacted into law in 1935. More than 65 million Americans receive a monthly check today, with retired employees accounting for 72 percent of the total. In addition, the program lifts nearly 22 million people out of poverty each year. What is going to happen to Beneficiaries? The cost-of-living adjustment (COLA) for 2022 came in at 5.9%, which all 65 million or so recipients were hoping to hear. In simpler terms, this means that at the start of January, all recipients will experience a 5.9% increase in their monthly payments. According to the Social Security Administration, this amounts to a $92 monthly boost for the average retired worker, bringing their total monthly income to $1,657. Overall, this 5.9% “increase” is the largest for Social Security recipients since 1983, and… Read more »

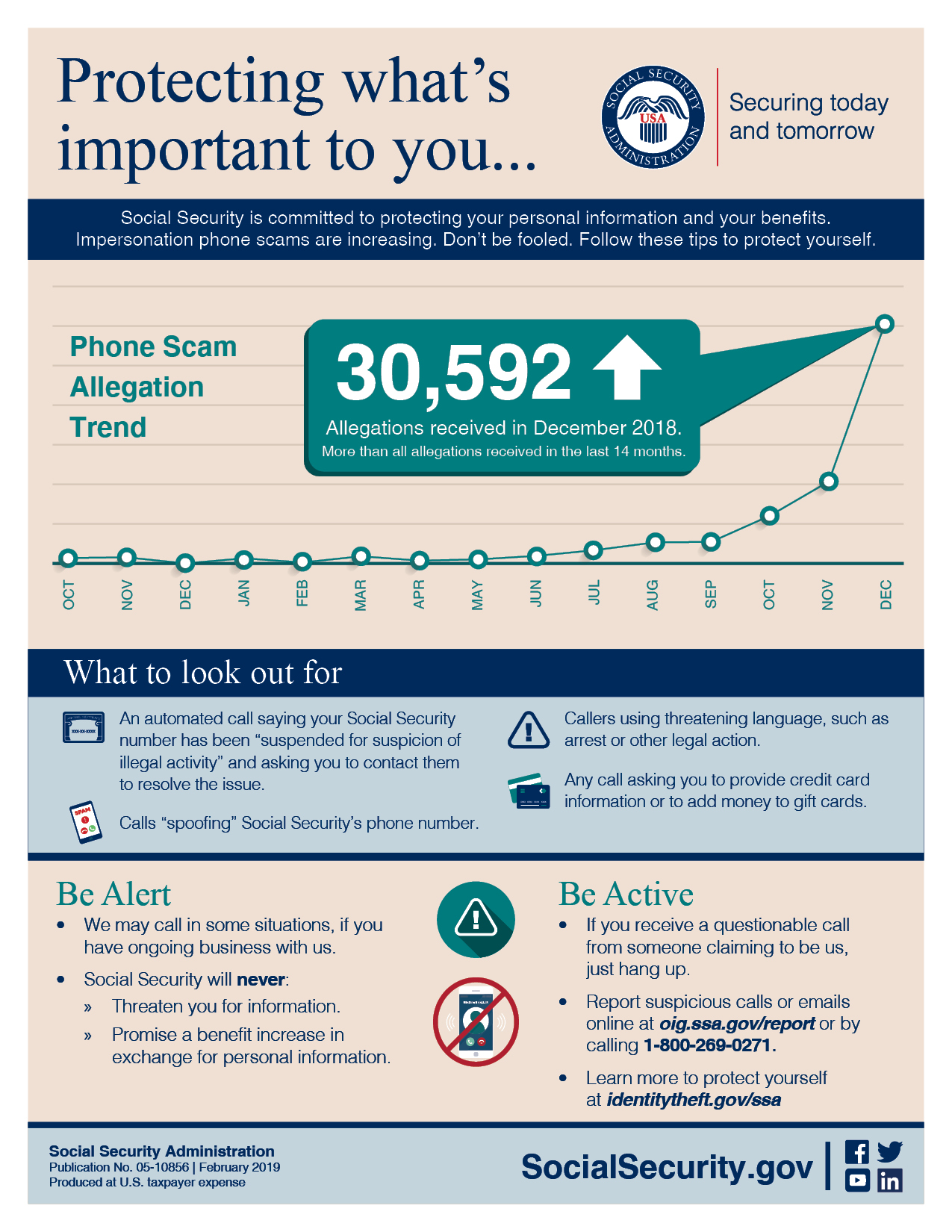

Social Security Fraud Calls & Scams – **ALERT** SSA Fraud Phone Calls On The Rise

Inspector General Warns About New Twist To Social Security Fraud Phone Call Scams Social Security phone call scams are the #1 type of fraud reported to the Federal Trade Commission and Social Security. Over the past year, these scams—misleading victims into making cash or gift card payments to avoid arrest for Social Security number problems—have skyrocketed. Latest Twist To Social Security Fraud Scams ***WARNING*** Telephone scammers may send fake documents by email to convince victims to comply with their demands. The Social Security Administration Office of the Inspector General (OIG) has received reports of victims who received emails with attached letters and reports that appeared to be from Social Security or Social Security OIG. The letters may use official letterhead and government “jargon” to convince victims they are legitimate; they may also contain misspellings and grammar mistakes. This is the latest variation on Social Security phone scams, which continue to… Read more »

!!ALERT!! Social Security Phone Scams 2019

Please be aware that there has been a significant rise in “Social Security Phone Scams” in 2019. Fraudsters are calling individuals with a variety of claims in an effort to people to divulge private information such as Social Security Numbers. Other phone scams claim that individuals are in trouble with an agency such as the police or IRS in an attempt to scare people into divulging private information or even sending money to resolve the “issue”. WATCH THIS VIDEO TO LEARN MORE ABOUT THE RECENT SOCIAL SECURITY PHONE SCAMS IN 2019 *** IT IS GOOD PRACTICE TO NEVER GIVE YOUR PERSONAL INFORMATION (SSN) OR SEND MONEY TO ANYONE THAT HAS MADE AN UNSOLICITED PHONE CALL TO YOU. ***

How to: Change or Sign Up for Direct Deposit – Video

If you receive Social Security benefits and have a bank account, starting or changing your direct deposit information is quick, secure, and easy with a my Social Security account. Learn more at http://ow.ly/hxOr30o1WhT

How to: Open a my Social Security Account – Video

my Social Security is a secure account that puts you in control with access to your information anytime, anywhere. Setting up an account is quick, secure, and easy at https://www.ssa.gov/myaccount/

How to: Change your address – Video

If you are moving and receive Social Security benefits, changing your address is quick, secure, and easy with a my Social Security account. Learn more at http://ow.ly/c5cJ30o1Wns.

How To: Report Your Wages to Social Security – Video

If you are a Supplemental Security Income (SSI) or Social Security disability insurance (SSDI) beneficiary, it is important to report your wages to Social Security. This process is quick, secure, and easy with a my Social Security account. Simply log into your account at http://ow.ly/bvHS30o1Vql.

How To: Get a Benefit Verification Letter – Video

Do you know how to get an income verification letter or benefit verification letter from Social Security? Just log in to my Social Security to get instant access to your benefit verification letter. Learn more at http://ow.ly/M8JQ30o1W46.

Will I Still Receive Disability Benefits After My Trial Work Period Ends?

Once an applicant is approved to receive Social Security disability benefits, they might try to go back to work. A trial work period is given by the Social Security Administration (SSA) to those who are taking home benefit checks to encourage them to go back into the job market. A trial work period spans for a complete 9 months. During this window, designated applicants will still receive a monthly check by the SSA, but once the trial work period has ended your benefits may be suspended. Keep in mind, a trial work period spans for 9 months, yet only the months where you bring home more than $850 a month contributes toward your trial work period. This number is evaluated and adjusted each year by the SSA. So it is important that you verify your salary before beginning any form of work. Also, the months that contribute to your trial… Read more »

What You Need To Qualify For Social Security Disability Benefits

How Does The Social Security Administration Define A Disability? If you wish to qualify to earn Social Security disability benefits, you must meet the following criteria: Your condition must be considered severe. Not every condition is automatically viewed as severe. While severity is somewhat subjective, the Social Security Administration (SSA) typically distinguishes severe from non-severe by determining if the condition substantially impairs someone’s ability to complete normal daily tasks. This is measured in adults by evaluating their ability to complete work requirements. Whereas in children, the SSA evaluates their ability to complete daily tasks that otherwise healthy same age children should be able to perform. Your condition has to last at least one year or result in death. 12 months is the minimum duration that a condition must last to qualify for Social Security Disability Insurance (SSDI) or Supplemental Security Income (SSA). If your condition is considered severe and disabling but… Read more »